")

Driving a car brings an immense sense of freedom, but it also comes with legal and financial responsibilities. In India, driving a motor vehicle without a valid insurance policy is a severe legal offense under the Motor Vehicles Act.

With the rapid progression of digital insurance ecosystems in 2026, renewing your policy is no longer a tedious process involving piles of paperwork or agent visits. Thanks to instantaneous e-KYC integration, unified regulatory portals, and personalized digital insurers, you can safely renew your car insurance online in under two minutes.

This comprehensive step-by-step guide walks you through the modern online renewal process, ensuring you secure maximum coverage at the best possible price.

Why You Should Never Let Your Car Insurance Lapse

Allowing your car insurance to expire even by a single day can expose you to hefty penalties and severe financial risks:

- Legal Consequences: Getting caught with a lapsed policy will result in steep traffic fines, vehicle impoundment, or even license suspension.

- Loss of No Claim Bonus (NCB): Your NCB is a hard-earned reward discount given for claim-free years, racking up to 50% off your own-damage premium. If your policy lapses and isn’t renewed within a strict window, your accumulated NCB drops back to zero.

- Higher Re-inspection Costs: Lapsed policies often trigger automated mandatory inspections, pushing your premium upward and delaying your security coverage.

Step-by-Step Guide to Renewing Car Insurance Online

Follow this quick, streamlined sequence to complete your renewal safely:

Step 1: Gather Your Vehicle Information

Before launching an insurance platform, ensure you have these digital details handy:

- Vehicle Registration Number & Chassis Number.

- Previous Year’s Insurance Policy Number.

- Any past claims information or your current accrued No Claim Bonus (NCB) percentage.

Step 2: Compare Quotes Online

Do not blindly stick to your existing insurer without exploring options. Use trusted Web Aggregators or Insurance Portals to pull comparative data across top providers. Compare policies based on:

- Incurred Claim Ratio (ICR): Shows the percentage of claims successfully settled by the insurer. Look for companies with an ICR above 85%.

- Network Garages: Ensure the insurer supports a vast network of cashless service garages in your immediate vicinity.

Step 3: Select the Right Policy Type

In 2026, you primarily have three digital paths to choose from:

- Third-Party Liability Cover: This is the mandatory legal baseline. It covers damage or injury caused by your car to another individual or property but provides zero financial protection for your own car.

- Comprehensive Car Insurance: The highly recommended shield. It bundles mandatory third-party liability with complete protection for your vehicle against accidents, theft, fire, and natural disasters.

- Pay-As-You-Drive (Usage-Based Cover): This model tracking via integrated telematics or smartphone apps allows you to pay premiums calculated directly on the exact kilometers you drive annually—perfect for remote workers or occasional drivers.

Step 4: Pick Essential Smart Add-ons

Customize your comprehensive policy with specific riders that can save thousands in out-of-pocket expenses:

- Zero Depreciation (Bumper-to-Bumper): Ensures the surveyor does not deduct depreciation costs on plastic, rubber, or glass components during a claim settlement.

- Engine Protection Cover: Essential if you live in flood-prone areas, safeguarding against severe water-logging or hydrostatic-lock damages.

- Roadside Assistance (RSA): Delivers immediate support for breakdowns, towing, flat tires, or running out of fuel.

Step 5: Complete e-KYC and Secure Payment

Input your updated details and select any applicable safety hardware declarations (like an approved anti-theft device) to slash your rates further. Confirm your identity effortlessly via biometric or Aadhaar-based e-KYC verification. Finally, make your premium payment via safe channels such as UPI, Credit Card, or Net Banking.

Step 6: Download Your Digital Policy Instantaneously

Upon successful payment routing, your digital policy document will be generated instantly. A certified soft copy will arrive in your e-mail inbox and sync seamlessly with your government-approved DigiLocker or mParivahan application for instant road verification.

Pro-Tips to Save Money on Car Insurance Online

Want to drop your 2026 premium even lower? Try incorporating these proven strategies into your next quote session:

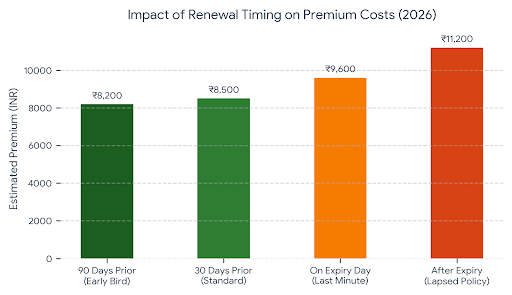

1. Renew Early to Freeze Rates

Do not wait until the final hour. Shopping for quotes 15 to 30 days before your actual expiry prevents last-minute stress, bypasses surprise pricing changes, and keeps your record meticulously clean.

2. Opt for Voluntary Deductibles

A voluntary deductible is the specific base amount you willingly agree to pay out of your pocket before the insurance coverage kicks in during a claim. Choosing a higher voluntary deductible directly drops your overall annual premium cost. (Note: Only do this if you are a confident driver who rarely makes claims).

3. Maintain a Immaculate Driving Record

Modern insurance tech leverages driver history and telematics scores to dynamically adjust premiums. Staying disciplined on the road prevents premium hikes and rewards you with premium-tier pricing.

Final Takeaway: Online car insurance renewal is a fast, safe, and transparent gateway to complete peace of mind. By spending just ten minutes comparing policies online, selecting high-utility add-ons, and utilizing usage-based parameters, you can easily save a huge chunk of money while protecting your favorite asset.

Leave a Reply